When the IRS added the crypto question to Form 1040 Schedule 1 it got crypto investors worried – not to fear, this blog should answer any questions you may have.

So did you (a) receive (as a reward, award, or payment for property or services); or (b) sell, exchange, or otherwise dispose of a digital asset (or a financial interest in a digital asset)??

Your reading this blog - so we’ll assume yes!

Although in the US specific tax rules do not exist for digital assets, for tax purposes a digital asset is (mainly) treated in the same way as property. Any time you dispose of a cryptocurrency (that is by selling, trading or paying for a service or goods) you are subject to capital gains or losses and we’ll take you through how to work this out.

Buy and Hold

If you only bought or held crypto, you haven't triggered a taxable event but should still, mark "yes" to inform the IRS of your ownership and the potential of capital gains if you dispose in the future. Optionally you could provide more details by attaching a statement or Form 8275.

So, calculating capital gains and losses…

Your gain/loss will be the difference between your adjusted basis in the virtual currency and the amount you received in exchange for it.

Capital Gain – if your purchased property increases in value then the profit generated from its disposal realizes a capital gain.

Capital Loss – If you dispose of property for less than your cost basis it is classed as a loss. This can be deducted from any capital gains for the tax year.

Capital gains calculation

Capital gains = selling price – purchase price (cost basis)

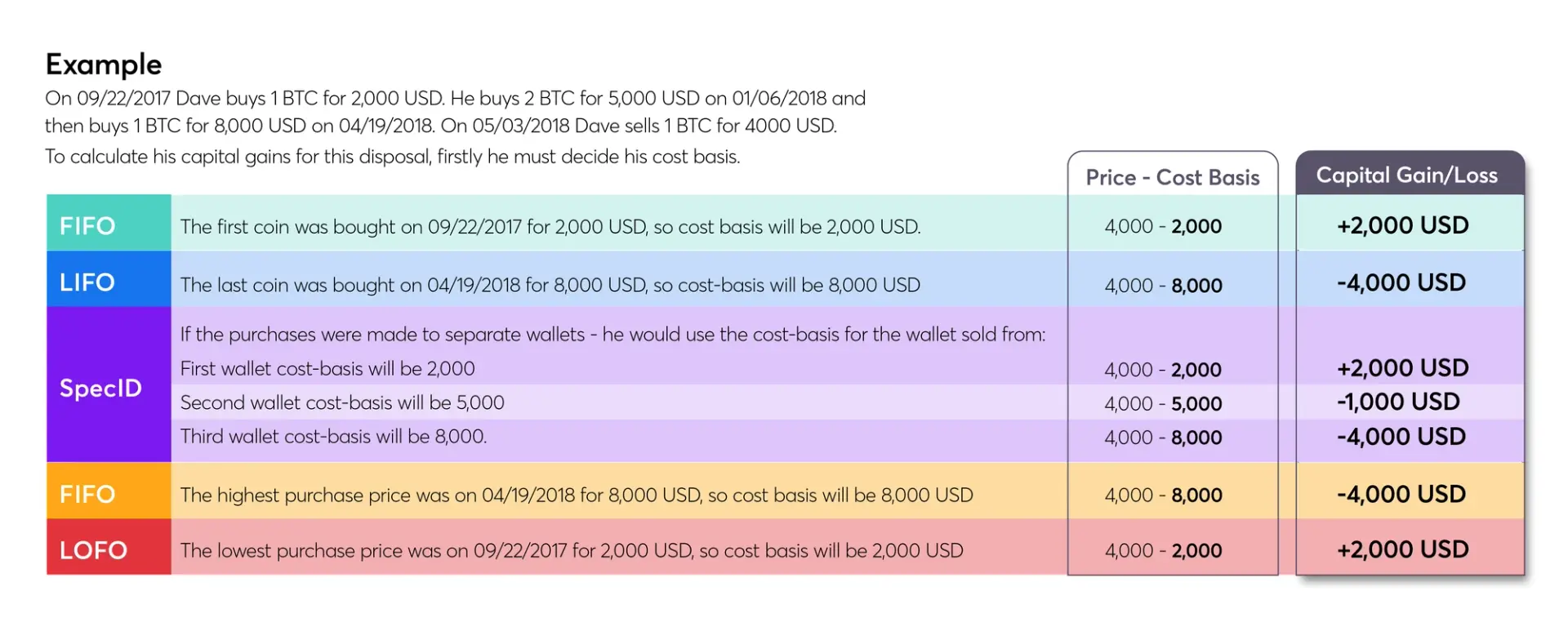

This seems pretty simple in theory, but it can get complicated... How do you determine your cost basis? If you have bought cryptocurrency at different times and at different prices how do you decide which you sold? There are a couple of different approaches...

FIFO First In First Out

(Preferred by the IRS) Assumes that the first assets you purchased are the first assets you sold or exchanged. So using this method your gains are calculated using the price paid for the oldest assets in your portfolio, and the asset price at the time of disposal.

LIFO Last In First Out

Assumes the last assets you bought are the first assets you sold or exchanged. Using this method your gains are calculated by using the price you paid for the most recently purchased assets and the asset price at time of disposal.

SpecID

This method can be used alongside FIFO/LIFO to give more control. The investor specifies the assets they sold or exchanged to determine the cost basis.

HIFO Highest In First Out

Calculated using the highest purchase price first, generating the lowest total gain.

LOFO Lowest In First Out

Calculates this highest total gain by using the lowest purchase price first.

Each method impacts your capital gains differently, which you can see in the example below.

The IRS are known to prefer the FIFO approach, although providing you stick to a consistent method throughout they are normally satisfied. However, you should get advice from a tax professional if not using the FIFO method or if you decide to change approach.

How Recap can help

You must calculate gain/loss for each individual disposal throughout the whole year so for those crypto investors/traders with lots of transactions it can be a very tedious and time demanding process. Recap manages your cryptocurrency data and calculates your gain/loss based on your chosen cost basis approach. You can download a ready to file tax report and file yourself or you can pass your report to your CPA and they will be able to complete the tax return and advise on your tax circumstance.

Where to report your capital gains

Once you have calculated your capital gains/losses they should be reported on Form 8949 and Form 1040 (Schedule D) of the tax return.

Form 8949

Form 8949 lists all of your transactions with date acquired, date of disposal, proceeds, cost basis and gain/loss. At the bottom of this form you should state your total proceeds, cost basis and gain/loss.

Form 1040 Schedule D

Form 1040 Schedule D summarizes your capital gains/losses taking into account if they were held short or long term.

How much tax will I owe?

The amount you'll have to pay Uncle Sam varies depending on how long you have held the crypto for and your income tax rate.

Short Term Capital Gains

- Cryptocurrency held for less than a year

- Taxed at your ordinary income rate

Long Term Capital Gains

- Cryptocurrency disposed of after a year

- Taxed at 0%, 15% or 20% dependent on income.

Income tax and cryptocurrency

Don’t forget that you'll also need to report any cryptocurrency income to the IRS. Any crypto that you have received but not “bought” is normally classed as income and should be reported under “Other Income” on Schedule 1 of your tax return.

Examples include:

- Receiving crypto instead of a fiat wage

- Income from mining

- Rewards – e.g. from staking, loans, ICO/IEOs, hard forks and airdrops

Hopefully, we’ve covered all of your questions but if you are in need of more detail then check out our full US Crypto Tax Guide.

Disclaimer

This guide is intended as a generic informative piece. This is not accounting or tax advice that can be relied upon for any UK individual’s specific circumstances. Please speak to a qualified tax advisor about your specific circumstances before acting upon any of the information in this article.